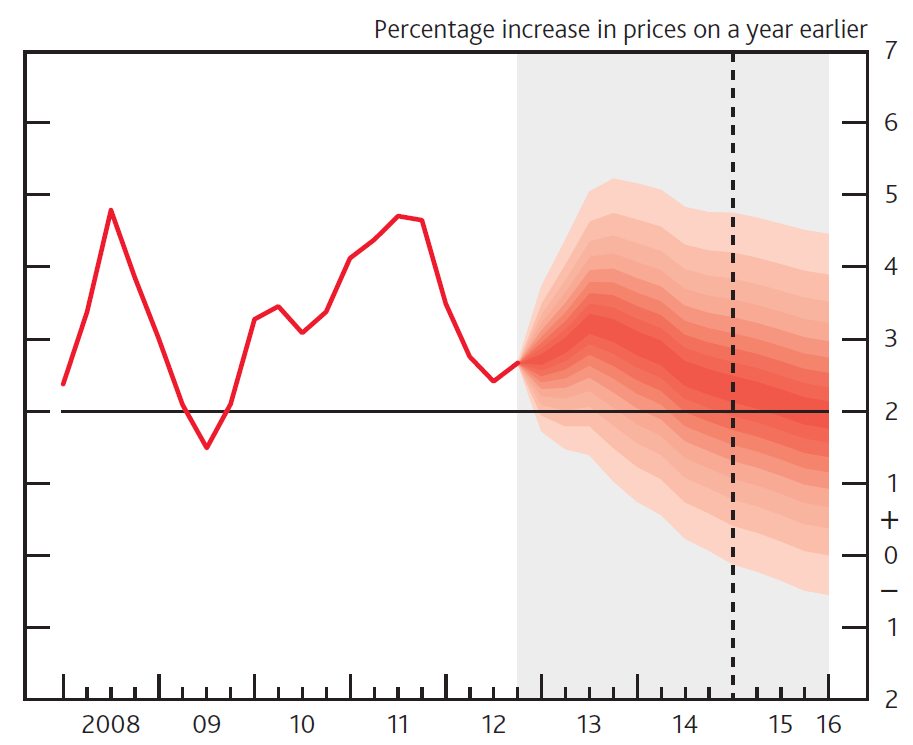

The Bank of England were one of the earliest pioneers of using fan charts to illustrate uncertainty in their forecasts, similar to this one:

As far as I can tell these charts were made in Excel, although (appropriately) I am not completely certain. There are also MATLAB scripts to create fan charts.

The fanplot package can also replicate Bank of England fan charts in R….

Split Normal (Two-Piece) Normal Distribution.

The Bank of England produce fan charts of forecasts for CPI and GDP in their quarterly Inflation Reports. They also provide data, in the form of mode, uncertainty and a skewness parameters of a split-normal distribution that underlie their fan charts (The Bank of England predominately refer to the equivalent, re-parametrised, two-piece normal distribution). The probability density of the split-normal distribution is given by Julio (2007) as

\[f(x; \mu, \sigma_1, \sigma_2) = \left\{\begin{array}{ll}\frac{\sqrt 2}{\sqrt\pi (\sigma_1+\sigma_2)} e^{-\frac{1}{2\sigma_1^2}(x-\mu)^2} \quad \mbox{for } -\infty < x \leq \mu \\\frac{\sqrt 2}{\sqrt\pi (\sigma_1+\sigma_2)} e^{-\frac{1}{2\sigma_2^2}(x-\mu)^2} \quad \mbox{for } \mu < x < \infty \\\end{array},\right.\]

where \(\mu\) represents the mode

parameter, and the two standard deviations \(\sigma_1\) and \(\sigma_2\) can be derived given the overall

uncertainty parameter, \(\sigma\) and

skewness parameters, \(\gamma\), as;

\(\sigma^2=\sigma^2_1(1+\gamma)=\sigma^2_2(1-\gamma).\)

The fanplot package contains functions for the density, distribution and

quantile of a split normal distribution (dsplitnorm,

psplitnorm and qsplitnorm) and a random

generator function rsplitnorm

Fan Chart Plots for CPI.

In order to reproduce the Bank of England plots there are two data

sets in the fanplot package. The cpi object is a time

series data frame with past values of CPI index. The boe

object is a data frame with historical details on the split normal

parameters for CPI inflation between Q1 2004 to Q4 2013 forecasts

published by the Bank of England.

## time0 time mode uncertainty skew

## 1 2004 2004.00 1.34 0.2249 0

## 2 2004 2004.25 1.60 0.3149 0

## 3 2004 2004.50 1.60 0.3824 0

## 4 2004 2004.75 1.71 0.4274 0

## 5 2004 2005.00 1.77 0.4499 0

## 6 2004 2005.25 1.68 0.4761 0The first column time0 refers to the base year of

forecast, the second, time indexes future projections,

whilst the remaining three columns provide values for the corresponding

projected mode (\(\mu\)), uncertainty

(\(\sigma\)) and skew (\(\gamma\)) parameters: Users can replicate

past Bank of England fan charts for a particular period after creating a

matrix object that contains values on the split-normal quantile function

for a set of user defined probabilities. For example, in the code below,

a subset of the Bank of England future parameters of CPI published in Q1

2013 are first selected. Then a vector of probabilities related to the

percentiles, that we ultimately would like to plot different shaded fans

for, are created. Finally, in a for loop the

qsplitnorm function, calculates the values for which the

time-specific (i) split-normal distribution will be less

than or equal to the probabilities of p.

# select relevant data

y0 <- 2013

boe0 <- subset(boe, time0==y0)

k <- nrow(boe0)

# guess work to set percentiles the BOE are plotting

p <- seq(0.05, 0.95, 0.05)

p <- c(0.01, p, 0.99)

# quantiles of split-normal distribution for each probability

# (row) at each future time point (column)

cpival <- matrix(NA, nrow = length(p), ncol = k)

for (i in 1:k)

cpival[, i] <- qsplitnorm(p, mode = boe0$mode[i], sd = boe0$uncertainty[i], skew = boe0$skew[i])The new object cpival contains the values evaluated from

the qsplitnormfunction in 6 rows and 13 columns, where rows

represent the probabilities used in the calculation p and

columns represent successive time periods.

cpival[1:5, 1:5]## [,1] [,2] [,3] [,4] [,5]

## [1,] 1.310928 0.8728139 0.6377539 0.1755382 -0.1673062

## [2,] 1.726639 1.4725288 1.3942125 1.0410359 0.7458961

## [3,] 1.948254 1.7922346 1.7974778 1.5024295 1.2327209

## [4,] 2.097776 2.0079386 2.0695589 1.8137296 1.5611793

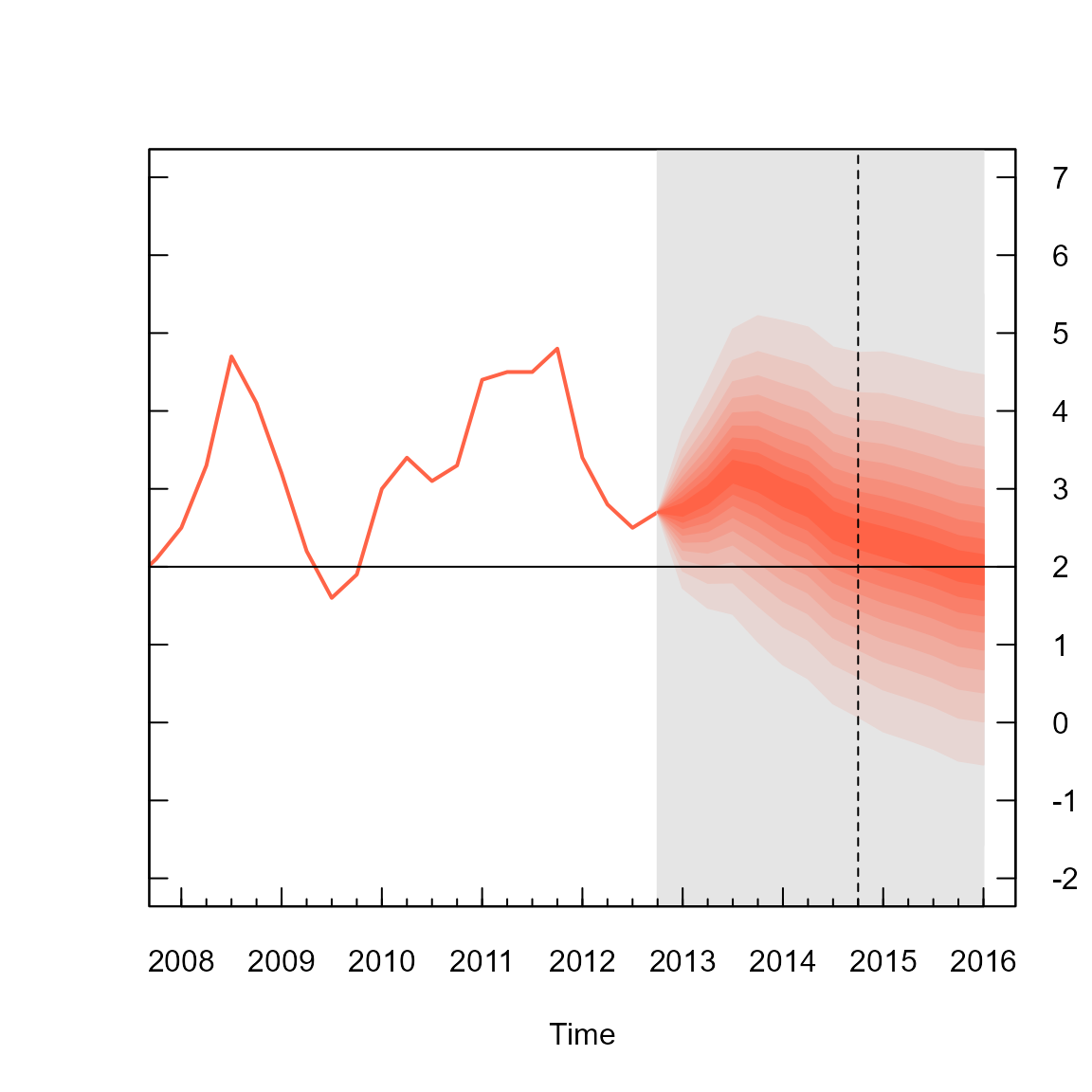

## [5,] 2.216611 2.1793733 2.2858004 2.0611410 1.8222275The object cpival can be used to add a fan chart to the

active R graphic device. In the code below, the area of the plot is set

up when plotting the past CPI data, contained in the time series object

cpi. The xlim arguments are set to ensure

space on the right hand side of the plotting area for the fan. Following

the Bank of England style for plotting fan charts, the background for

future values is set to a gray colour, y-axis are plotted on the right

hand side, a horizontal line are added for the CPI target and a vertical

line for the two-year ahead point.

# past data

plot(cpi, type = "l", col = "tomato", lwd = 2,

xlim = c(y0 - 5, y0 + 3), ylim = c(-2, 7),

xaxt = "n", yaxt = "n", ylab="")

# background

rect(y0 - 0.25, par("usr")[3] - 1, y0 + 3, par("usr")[4] + 1, border = "gray90", col = "gray90")

# add fan

fan(data = cpival, data.type = "values", probs = p,

start = y0, frequency = 4,

anchor = cpi[time(cpi) == y0 - 0.25],

fan.col = colorRampPalette(c("tomato", "gray90")),

ln = NULL, rlab = NULL)

# boe aesthetics

axis(2, at = -2:7, las = 2, tcl = 0.5, labels = FALSE)

axis(4, at = -2:7, las = 2, tcl = 0.5)

axis(1, at = 2008:2016, tcl = 0.5)

axis(1, at = seq(2008, 2016, 0.25), labels = FALSE, tcl = 0.2)

abline(h = 2) #boe cpi target

abline(v = y0 + 1.75, lty = 2) #2 year line

The fan chart itself is outputted from the fan function,

where arguments are set to ensure a close resemblance of the R plot to

that produced by the Bank of England. The first three arguments in the

fan function called in the above code, provide the

cpival data to plotted, indicate that the data are a set of

calculated values (as opposed to simulations) and provide the

probabilities that correspond to each row of cpival object.

The next two arguments define the start time and frequency of the data.

These operate in a similar fashion to those used when defining time

series in R with the ts function. The anchor

argument is set to the value of CPI before the start of the fan chart.

This allows a join between the value of the Q1 2013 observation and the

fan chart. The fan.col argument is set to a colour palette

for shades between tomato and gray90. The

final two arguments are set to NULL to suppress the

plotting of contour lines at the boundary of each shaded fan and their

labels, as per the Bank of England style.

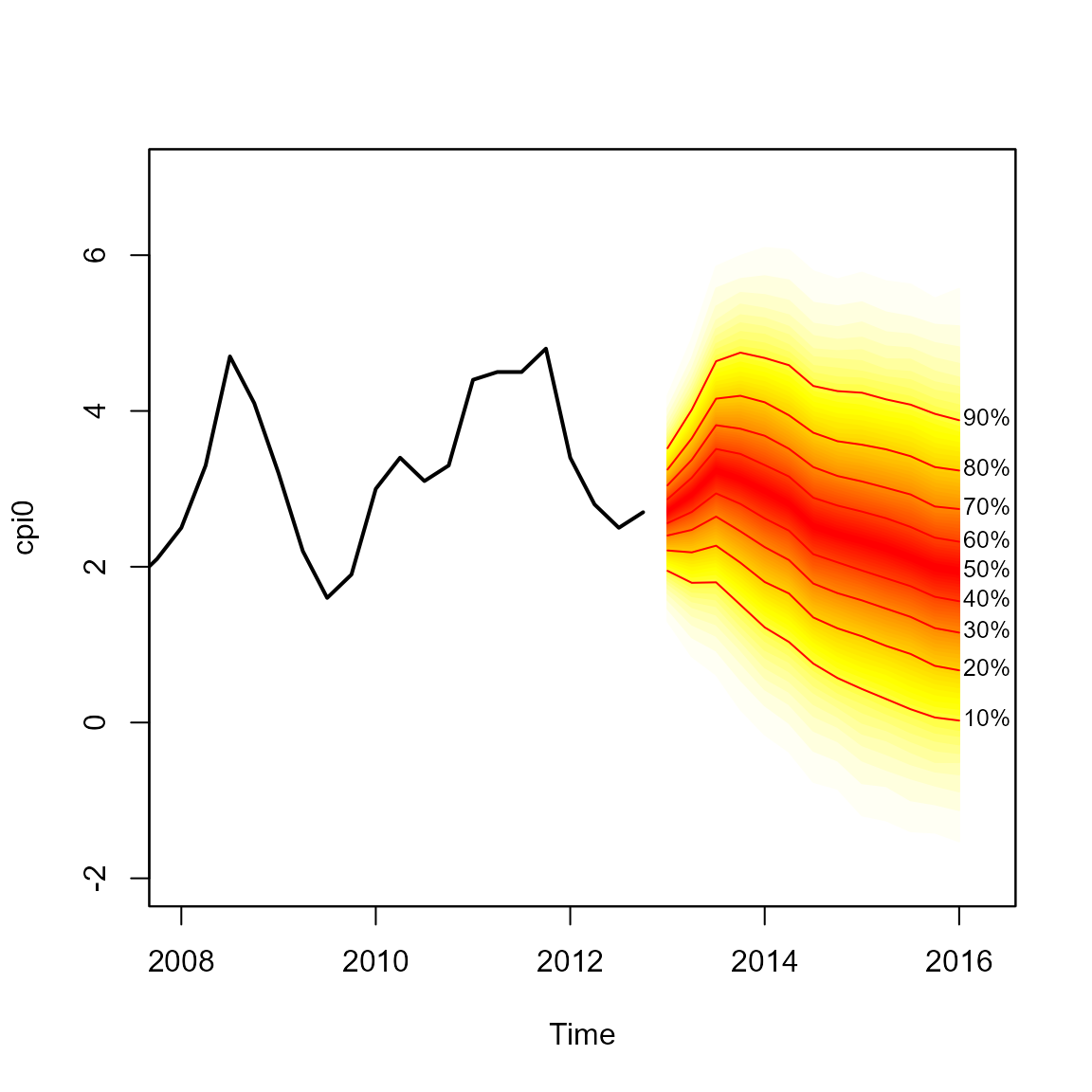

Default Fan Chart Plot.

By default, the fan function treats objects passed to

the data argument as simulations from sequential

distributions, rather than user-created values corresponding

probabilities provided in the probs argument (as above). An

alternative plot below, based on simulated data and default style

settings in the fan function produces a fan chart with a

greater array of coloured fans with labels and contour lines alongside

selected percentiles of the future distribution. To illustrate we can

simulate 10,000 values from the future split-normal distribution

parameters from Q1 2013 in the boe0 data frame using the

rsplitnormfunction

#simulate future values

cpisim <- matrix(NA, nrow = 10000, ncol = k)

for (i in 1:k)

cpisim[, i] <- rsplitnorm(n = 10000, mode = boe0$mode[i], sd = boe0$uncertainty[i], skew = boe0$skew[i])The fan chart based on the simulations in cpisim can

then be added to the plot;

# truncate cpi series

cpi0 <- ts(cpi[time(cpi)<2013], start=start(cpi), frequency=frequency(cpi) )

# past data

plot(cpi0, type = "l", lwd = 2, xlim = c(y0 - 5, y0 + 3.25), ylim = c(-2, 7))

# add fan

fan(data = cpisim, start = y0, frequency = 4)

The fan function calculates the values of 100 equally

spaced percentiles of each future distribution when the default

data.type = "simulations" is set. This allows 50 fans to be

plotted from the heat.colours colour palate, providing a

finer level of shading in the representation of future distributions. In

addition, lines and labels are provided along each decile. The fan chart

does not connect to the last observation as anchor = NULL

by default.