1000 MCMC Simulations of Estimated Volatility from Pound–Dollar Exchange Rate Data

Source:R/th_mcmc.R

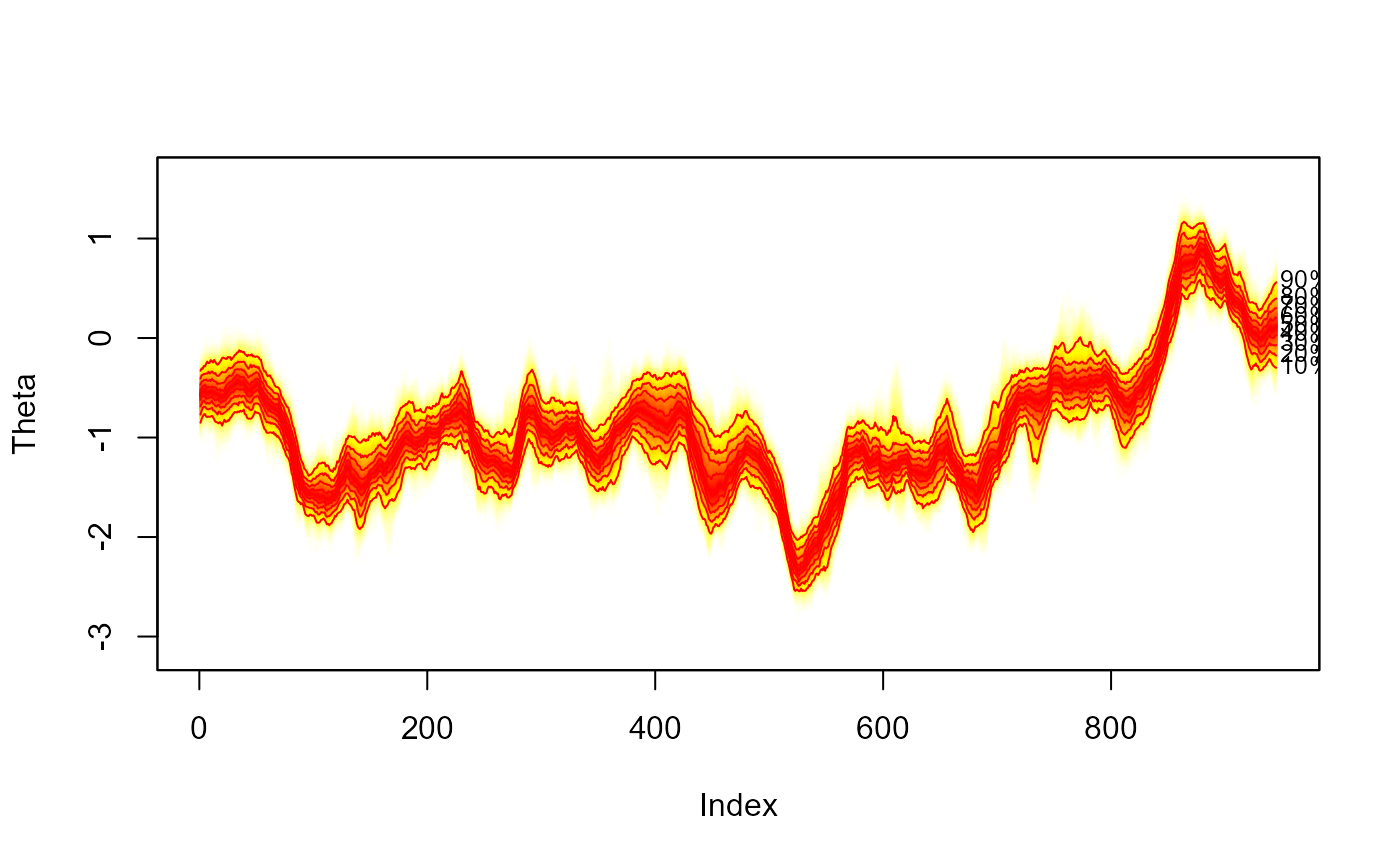

th.mcmc.RdMCMC simulations of volatility obtained from the bugs function in the

R2OpenBUGS package. Estimates are based on the stochastic volatility model for

Pound–Dollar exchange rate data presented in the appendix of Meyer and Yu (2002).

The MCMC was run for 1100 simulations, thinning to keep every 10th iteration,

and treating the first 100 simulations as burn-in.

Usage

data(th.mcmc)Details

Larger simulations (without thinning) can be obtained using the data

(svpdx) and the my1.txt BUGS file contained in this package;

see the example below.

See Meyer and Yu (2010) for model specification.

References

Meyer, R. and J. Yu (2002). BUGS for a Bayesian analysis of stochastic volatility models. Econometrics Journal, 3(2), 198–215.

Sturtz, S., U. Ligges, and A. Gelman (2005). R2WinBUGS: a package for running WinBUGS from R. Journal of Statistical Software, 12(3), 1–16.

Examples

# empty plot

plot(NULL, type = "n", xlim = c(1, 945),

ylim = range(th.mcmc), ylab = "Theta")

# add fan

fan(th.mcmc)

## Create your own (longer) MCMC sample:

# \dontrun{

# library(tsbugs)

# library(R2OpenBUGS)

#

# # write model file:

# my1.bug <- dget(system.file("model", "my1.R", package = "fanplot"))

# write.model(my1.bug, "my1.txt")

#

# # take a look:

# file.show("my1.txt")

#

# # run OpenBUGS (include theta as a parameter or nothing will be plotted)

# my1.mcmc <- bugs(

# data = list(n = length(svpdx$pdx), y = svpdx$pdx),

# inits = list(list(phistar = 0.975, mu = 0, itau2 = 50)),

# param = c("mu", "phi", "tau", "theta"),

# model = "my1.txt",

# n.iter = 11000, n.burnin = 1000, n.chains = 1

# )

#

# th.mcmc <- my1.mcmc$sims.list$theta

# }

## Create your own (longer) MCMC sample:

# \dontrun{

# library(tsbugs)

# library(R2OpenBUGS)

#

# # write model file:

# my1.bug <- dget(system.file("model", "my1.R", package = "fanplot"))

# write.model(my1.bug, "my1.txt")

#

# # take a look:

# file.show("my1.txt")

#

# # run OpenBUGS (include theta as a parameter or nothing will be plotted)

# my1.mcmc <- bugs(

# data = list(n = length(svpdx$pdx), y = svpdx$pdx),

# inits = list(list(phistar = 0.975, mu = 0, itau2 = 50)),

# param = c("mu", "phi", "tau", "theta"),

# model = "my1.txt",

# n.iter = 11000, n.burnin = 1000, n.chains = 1

# )

#

# th.mcmc <- my1.mcmc$sims.list$theta

# }