Visualising Time Series Model Results

The fanplot package is designed to help display uncertainty in

estimates from time series models. To illustrate, the packages

th.mcmc data frame object contains posterior density

distributions of the estimated volatility of daily returns \(y_t\) from the Pound/Dollar exchange rate

from 02/10/1981 to 28/6/1985. These distributions are from a MCMC

simulation from a stochastic volatility model given in

Meyer

and Yu (2002) where it assumed;

\[ y_t | \theta_t = \exp\left(\frac{1}{2}\theta_t\right)u_t \qquad u_t \sim N(0, 1) \qquad t=1,\ldots,n. \]

The latent volatilities \(\theta_t\), which are unknown states in a state-space model terminology, are assumed to follow a Markovian transition over time given by the state equations:

\[ \theta_t | \theta_{t-1}, \mu, \phi, \tau^2 = \mu + \phi \log \sigma^2_{t-1} + v_t \qquad v_t \sim N(0, \tau^2) \qquad t=1,\ldots,n \]

with \(\theta_0 \sim N(\mu, \tau^2)\).

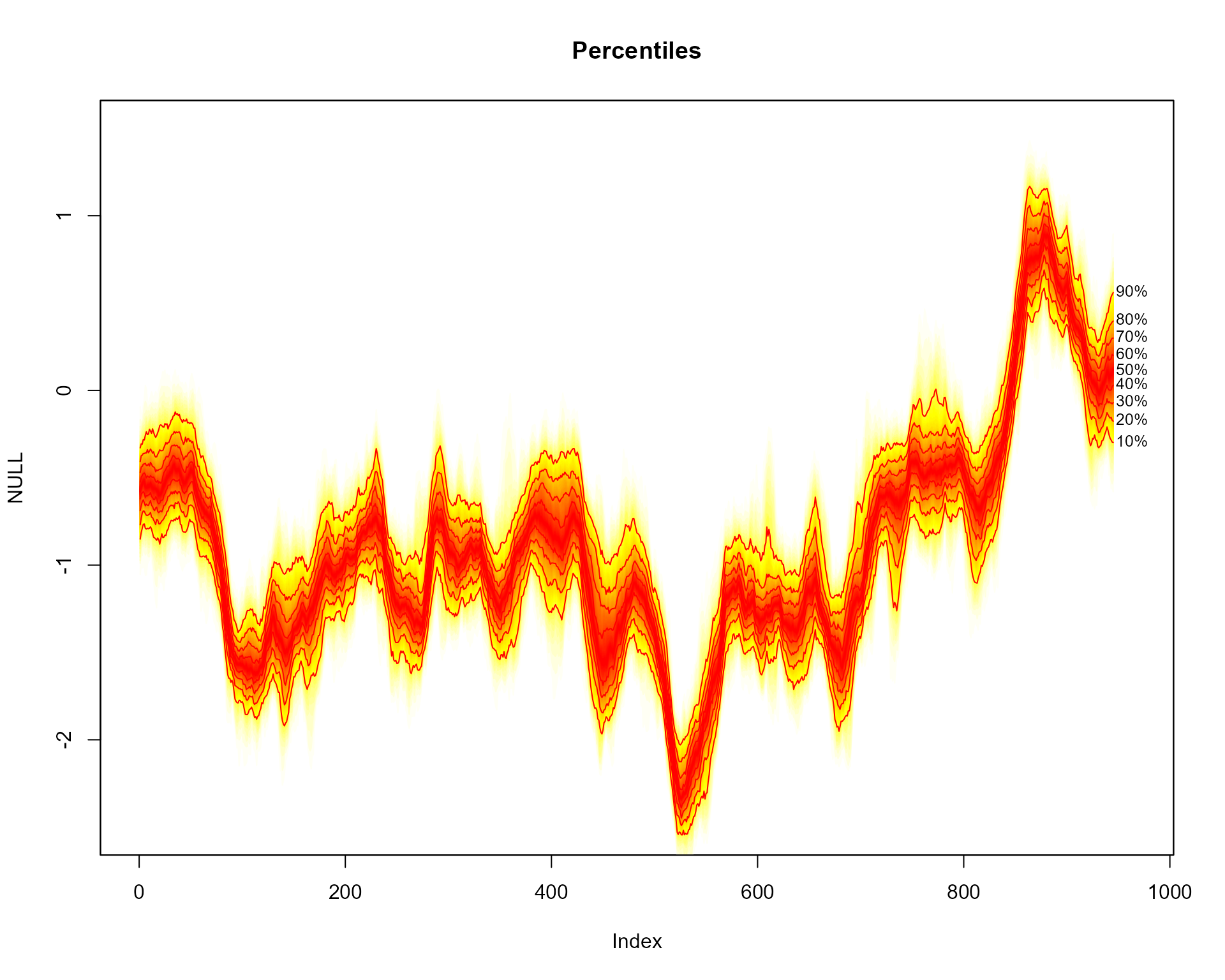

The th.mcmc object consists of (1000) rows corresponding

to MCMC simulations and (945) columns corresponding to each \(t\). A fan chart of the evolution of the

distribution of \(\theta_t\) can be

visualised using the fanplot package via,

library(fanplot)

# empty plot

plot(NULL, main="Percentiles", xlim = c(1, 965), ylim = c(-2.5, 1.5))

# add fan

fan(data = th.mcmc)

The fan() function calculates the values of 100 equally

spaced percentiles of each future distribution when the default

data.type = "simulations" is set. This allows 50 fans to be

plotted from the heat.colours colour palette, providing a

fine level of shading. In addition, lines and labels are provided along

each decile.

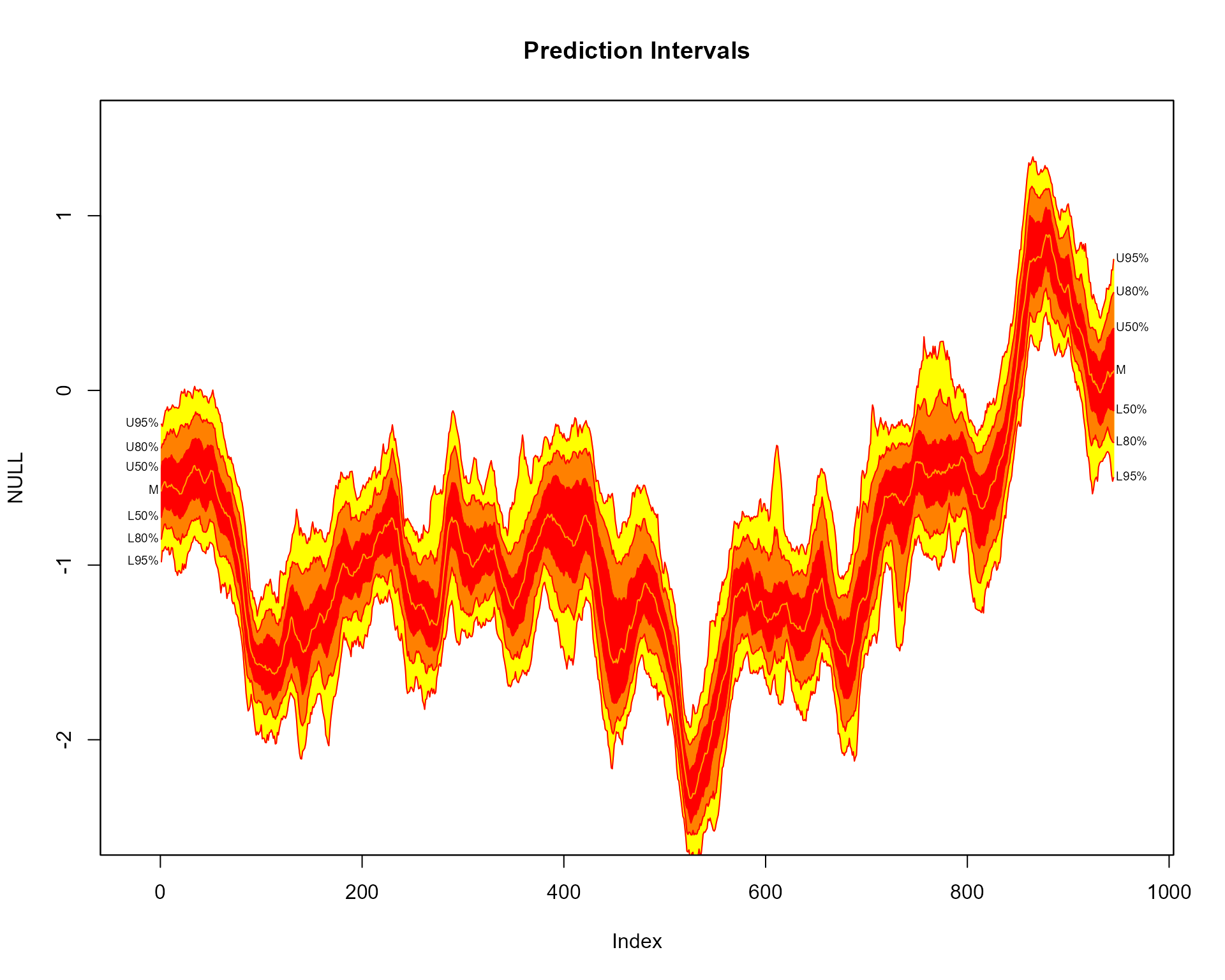

Prediction Intervals

When argument type = "interval" is set, the

probs argument corresponds to prediction intervals.

Consequently, the fan chart comprises of 3 different shades, running

from the darkest shade for the 50th prediction interval to the lightest

for the 95th prediction interval.

# empty plot

plot(NULL, main="Prediction Intervals", xlim = c(-20, 965), ylim = c(-2.5, 1.5))

# add fan

fan(data = th.mcmc, type = "interval", llab=TRUE, rcex=0.6)

Contour lines are overlayed for the upper and lower bounds of each

prediction intervals, as set using the ln command. A

further line is plotted along the median of \(\theta_t\), which is controlled by the

med.ln argument (set to TRUE by default when

type="interval"). The default labels on the right hand side

correspond to the upper and lower bounds of each plotted line. The left

labels are added by setting llab = TRUE. Note, some extra

room is created for the labels by setting the

xlim = c(-20, 965) argument of plotting area to a wider

range than the original data (945 observations). The text size of the

right labels are controlled using the rcex argument. The

left labels, by default, take the same text size as rcex

although they can be separately controlled using the lcex

argument.

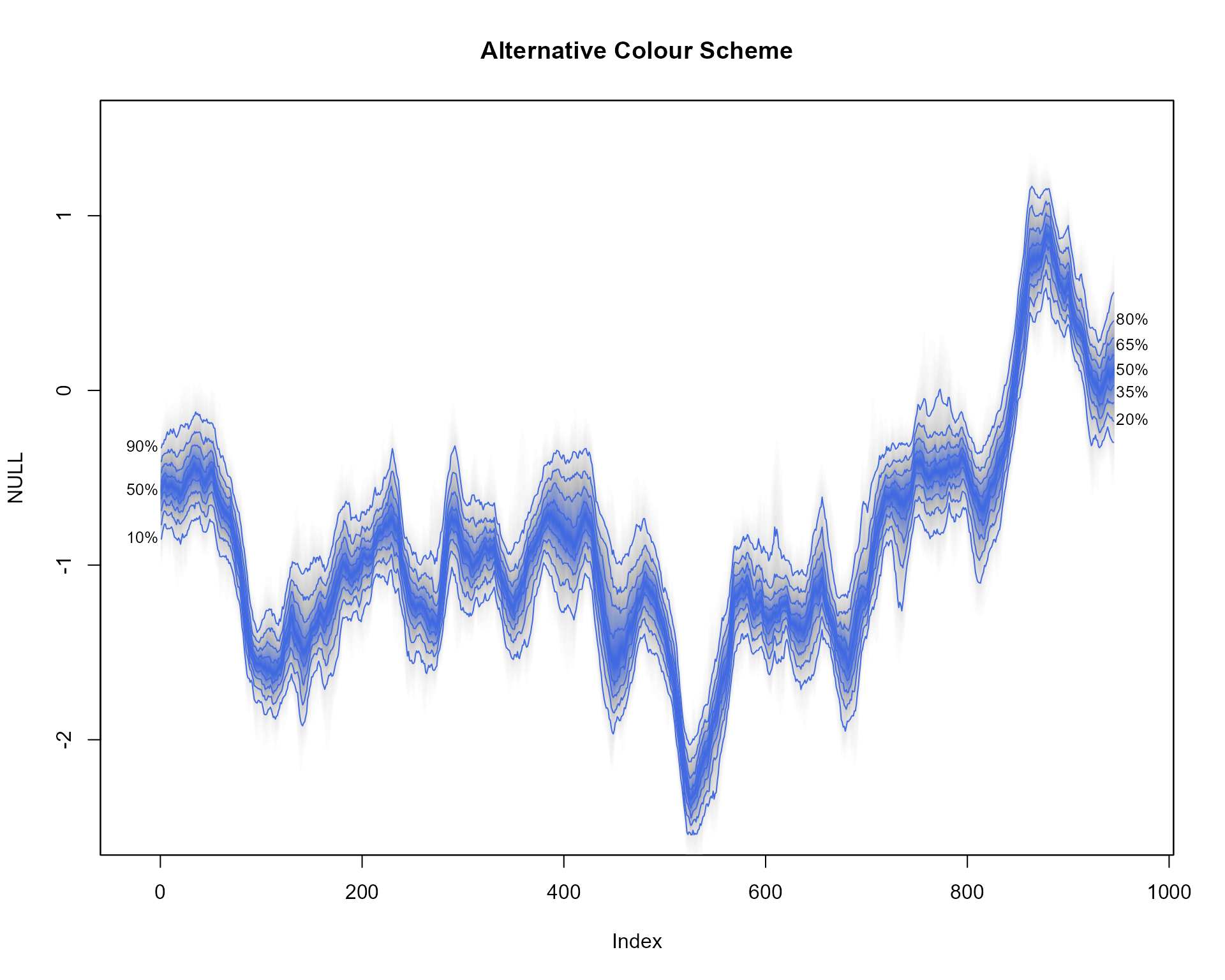

Alternative Colours

Alternative colour schemes to the default heat.colors,

can be obtained by supplying a colorRampPalette to the

fan.col argument. For example, a new palette running from

blue to white, via grey can be passed using;

# empty plot

plot(NULL, xlim = c(-20, 965), ylim = c(-2.5, 1.5), main="Alternative Colour Scheme")

# add fan

fan(data = th.mcmc, rlab=seq(20,80,15), llab=c(10,50,90), fan.col=colorRampPalette(c("royalblue", "grey", "white")))

Alternative labels are specified using the rlab and

llab arguments.

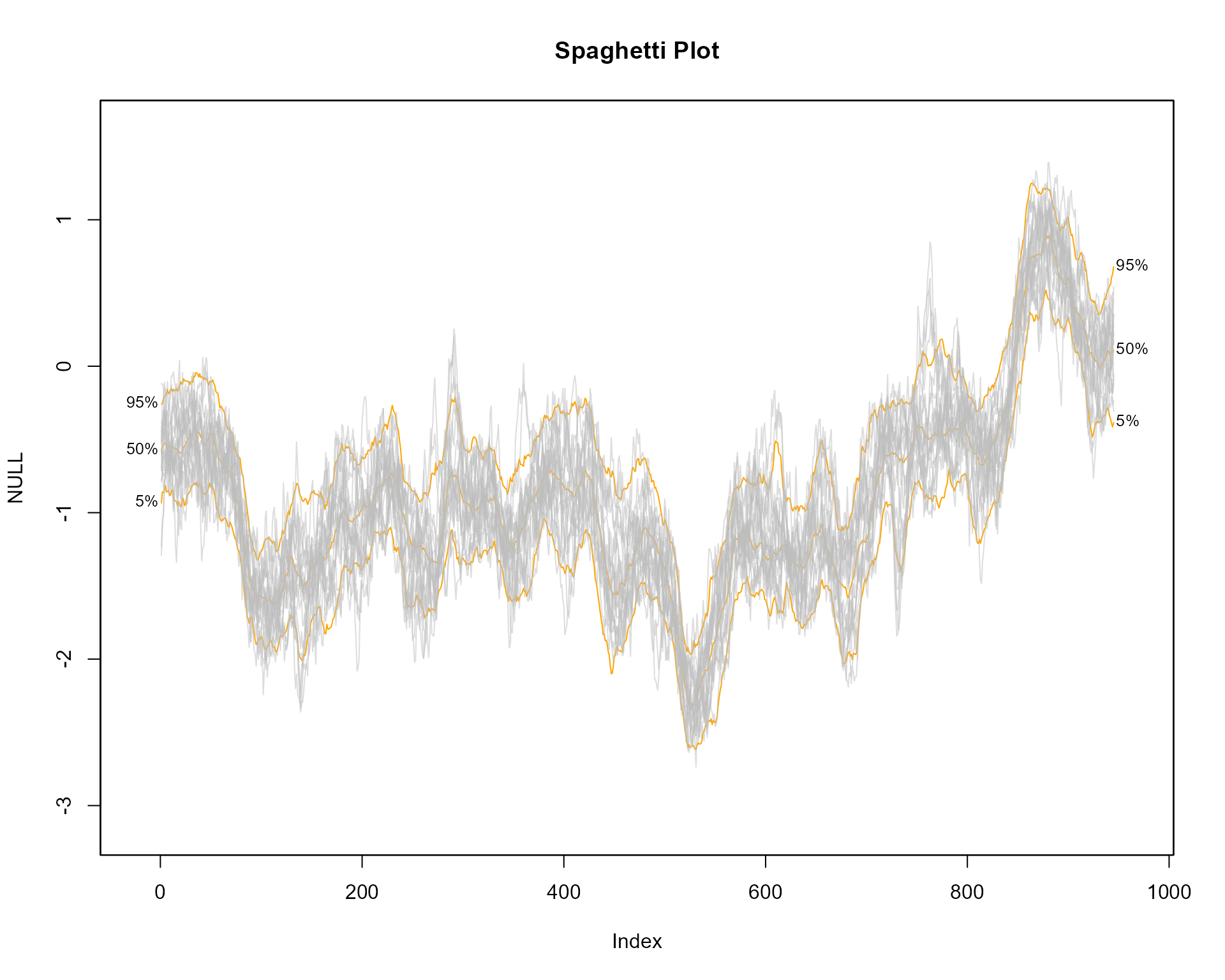

Spaghetti Plots

Spaghetti plots can be used to represent uncertainty shown by a range

of possible future trajectories or past estimates. For example using the

th.mcmc object, 20 random sets of \(\theta_t\) can be plotted when setting the

argument style = "spaghetti";

# empty plot

plot(NULL, main="Spaghetti Plot", xlim = c(-20, 965), ylim = range(th.mcmc))

# transparent fan with visible lines

fan(th.mcmc, ln=c(5, 50, 95), llab=TRUE, alpha=0, ln.col="orange")

# spaghetti lines

fan(th.mcmc, style="spaghetti", n.spag=20)

The spaghetti lines are superimposed on a fan chart in order to

illustrate some underlying probabilities. The initial fan chart is

completely transparent from setting the transparency argument

alpha to 0. In order for the percentile lines to be visible

a non-transparent colour is used for the ln.col

argument.

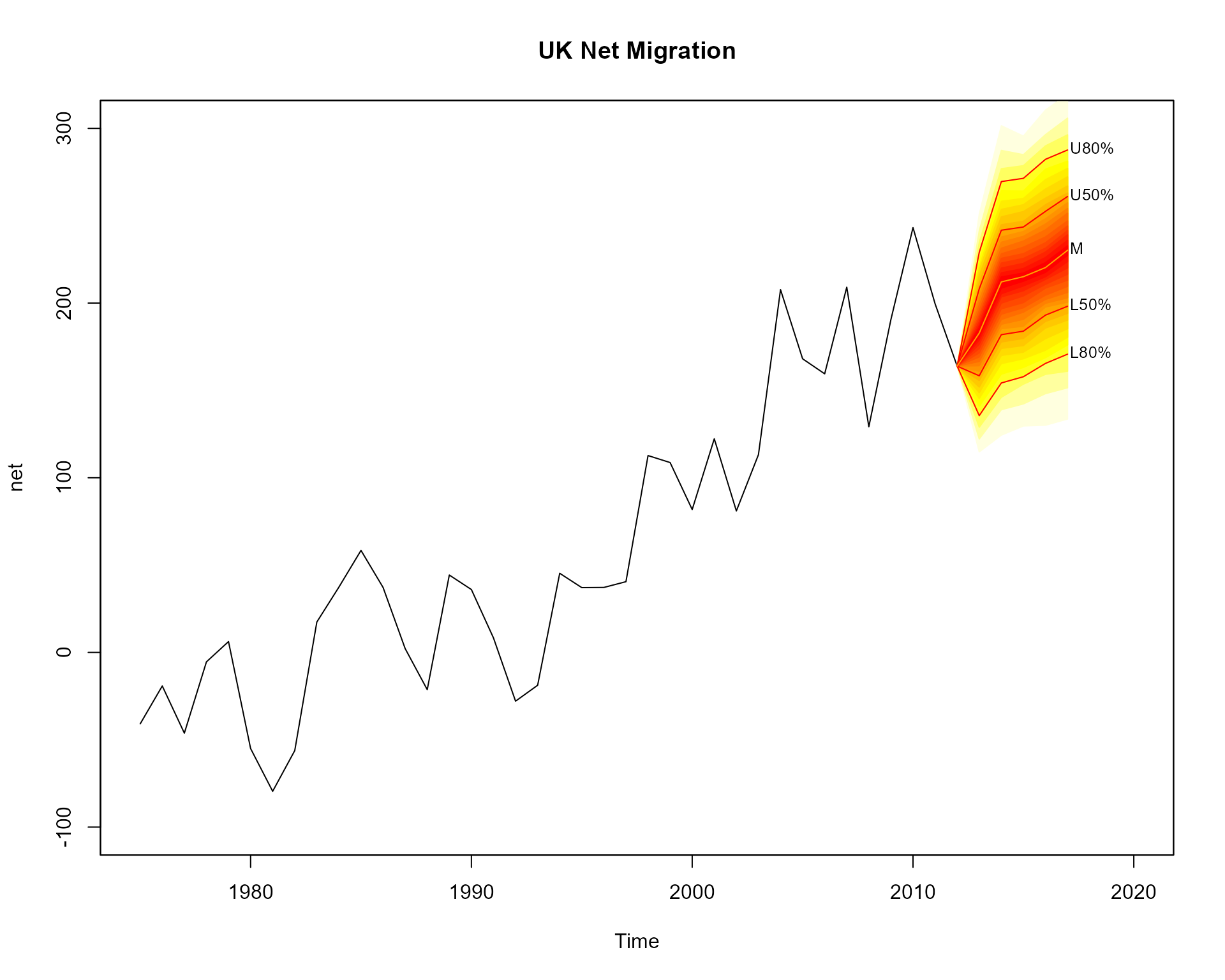

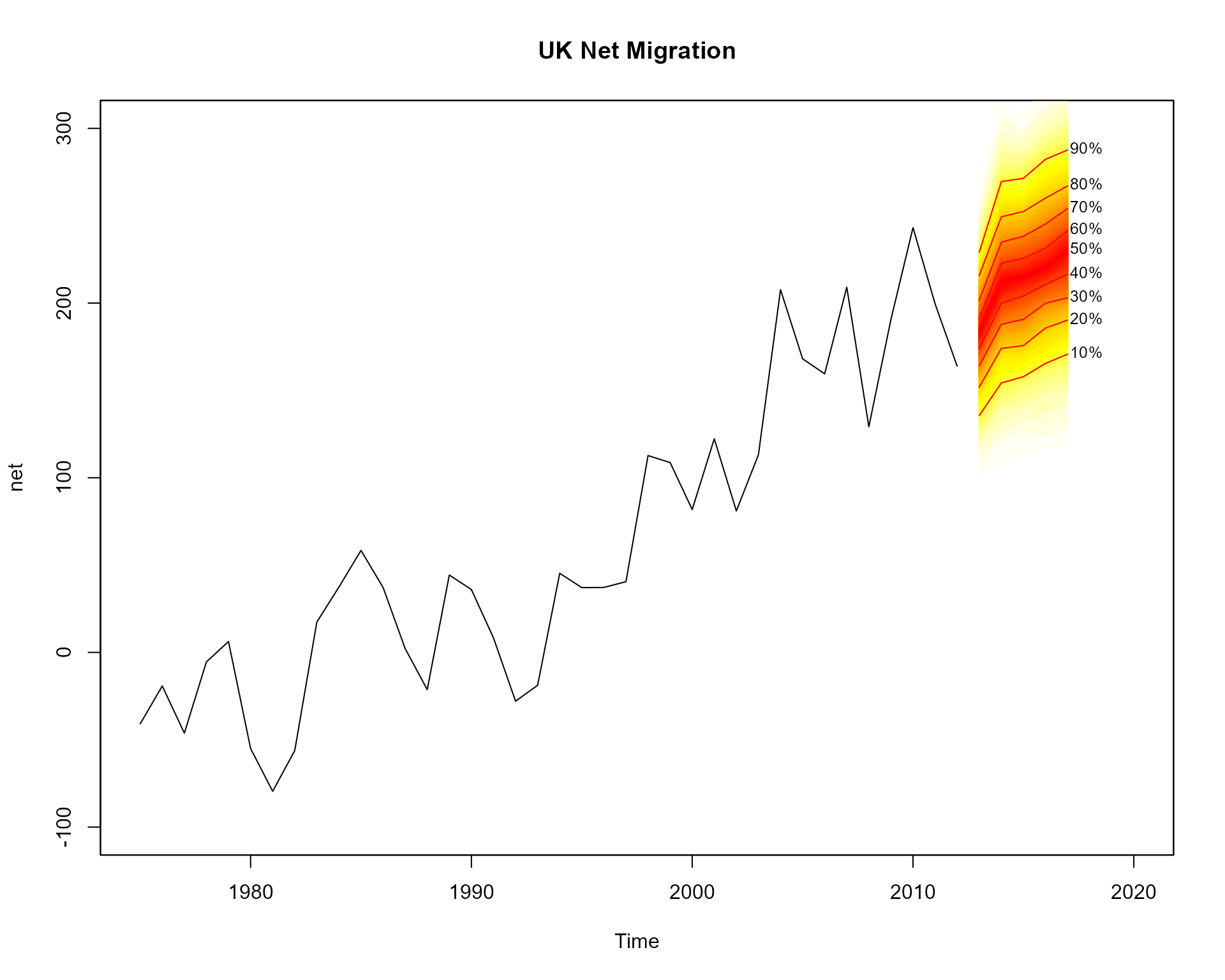

Forecast Fans

The fanplot package can also be used to illustrate probabilistic

forecasts. For example, using the auto.arima function in

the

forecast

package a model for the time series for net migration to the United

Kingdom (contained in the ips data frame of the fanplot

package) can be fitted.

#create time series

net <- ts(ips$net, start = 1975)

#fit model

library(forecast)

m <- auto.arima(net)

m## Series: net

## ARIMA(1,1,2) with drift

##

## Coefficients:

## ar1 ma1 ma2 drift

## -0.2301 -0.0851 -0.6734 6.7625

## s.e. 0.3664 0.3571 0.1898 1.3961

##

## sigma^2 = 1343: log likelihood = -184.28

## AIC=378.56 AICc=380.5 BIC=386.62We may then simulate 1000 values from the selected model using the

simulate.Arima function, and plot the results.

mm <- matrix(NA, nrow=1000, ncol=5)

for(i in 1:1000)

mm[i,] <- simulate(m, nsim=5)

# empty plot

plot(net, main="UK Net Migration", xlim=c(1975,2020), ylim=c(-100,300))

# add fan

fan(mm, start=2013)

Users might want to connect the fan with the past data. This can be

achieved by providing the last value to the anchor argument. More shades

for the fan are added to the plot (over the default 3 used for a

interval fans) by supplying a sequence to the probs

argument. Alternative contour lines (from the default median, 50th, 80th

and 95th percentiles for interval fans) are added using the

ln argument.

# empty plot

plot(net, main="UK Net Migration", xlim=c(1975,2020), ylim=c(-100,300))

# add fan

fan(mm, start=2013, anchor=net[time(net)==2012], type="interval", probs=seq(5, 95, 5), ln=c(50, 80))